Time builds relationships. But it also kills deals. (Investor Skydiving)

Building, sustaining, and closing investor interest

You see an investor you really like and really want to ask them to invest!

Hold your horses! Slow down. Take your time building relationships…

But also, if you think you have captured investor interest… don't drag your feet.

Why?

Because time kills deals.

Confused? Count yourself among endless numbers of other founders.

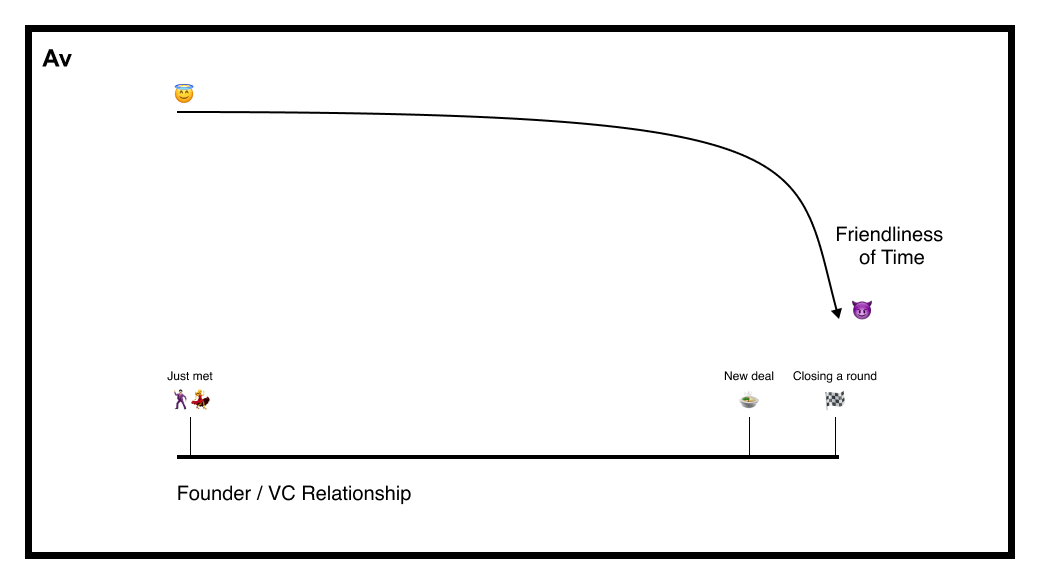

There is a head spinning relationship between time and your ability to close deals. In the beginning, you need to give ample time to generate enough interest where an investor will want to do a deal.

If you move too quickly, the investor may be turned off. If you push too hard and force an investor’s hand, you may mess things up and not generate enough interest to convert an investor.

On the other hand, when investors are excited about your business idea, it is best to close them quickly before you lose their interest.

It looks a bit like this:

Why is that?

On the front end – an investor is trying to determine how comfortable they are with a founder and how excited they are about a deal.

In an ideal scenario, investors grow comfort over a long-term relationship-building process. The more an investor learns about a founder, the more comfort builds and turns into anticipation.

Anticipation? For what?

When an investor meets a founder, they always wonder “Would I invest in her”? They don’t mean right this second. They mean at some point.

Venture capital is a long game driven by planting a ton of opportunity seeds of which a few will grow into deal opportunity sprouts and even fewer will become towering money trees!

So anticipation for what?

Well after that opportunity seed gets planted, something might begin to sprout. Perhaps the investor sees a deep passion for a space. Maybe they notice a unique expertise. Or maybe they see the founder actually executing towards their vision.

This is when a VC gets excited. They start seeing signs of a deal opportunity sprouting. They can’t tell exactly when, but there may be an opportunity to harvest a real deal. THIS is what they’re anticipating.

While time is your friend, this is what you’ll need to work towards creating. Anticipation for your deal.

But time will turn on you

Up till then, time is your friend. The more time you can spend cultivating relationships with VCs who will want you to turn into a deal opportunity the better.

The moment you launch an actual fundraise, time begins to turn on you. It is no longer patient. It becomes fickle and you need to tread lightly.

In those early days of a fundraise, structured amounts of time help organize investors into focusing on the opportunity. It can’t be too limited though because the investor needs enough time to get excited about the specific deal. It is a careful balancing act.

Time, the full-blown enemy

The final transition happens when the fundraise produces palpable excitement from at least 1 investor. Now time is fully your enemy.

Once you’ve hooked a fish, more time just means more data. And more data doesn't necessarily mean a better chance of closing. In fact, more data is likely to cause an investor to second guess her initial excitement. This is true at any stage but especially at the very earliest stages.

In this stage, time is your enemy. You have to control the process and drive it to its conclusion.

Time kills deals.

Investing, an action sport

So much of deal making and investment commitments are decided based on extrapolation of limited data, gut feeling, and an exciting acceptance of risk.

If a deal is priced competitively, there is always risk that you made a bad investment. Maybe the founder can't accomplish what she said she would. Maybe the asking price is too high and requires too much to grow into. That thrill and risk is what investors are betting on. That is the risk / return dynamic of venture investing. It feels like an action sport.

Investor Skydiving

I’ve described the time dynamic above to founders in the past, and it rarely resonates. Here’s my attempt to break through with an analogy.

Venture capital investing is like skydiving. VCs are the thrill seekers and founders are the skydiving company operators.

When an investor thinks about putting huge amounts of money into a risky investment, they are in a sense evaluating the exciting opportunity to jump out of a plane.

At the beginning they might hear about a new skydiving company. Someone told them that a new company has the COOLest new skydives. Does the investor rush and jump on the next plane?

Here’s a better question. If someone ran up to you and said “HEY BRAND NEW SKYDIVING COMPANY. FIRST TRIP IS TOMORROW. LET’S GO!” Would you go?

No, of course not. You’d want to find out more about the company. You’re risking your life… you need to be sure it’s reputable. The same goes with investor skydiving. Investors need to feel comfortable before jumping out of a plane with a founder.

Getting on the plane

Launching a fundraising process is like selling tickets to a skydive. If you’ve built enough reputation for your company, you’ll at least be able to sell them a ticket.

The safety presentation and equipment review are first meetings. Many people bail during this phase. Investors learn a little more about what they’re about to do …and they pass (bawk bawk 🐔).

If the founder has done what’s necessary to build reputation, and the first safety checks and pump up conversations go well, they will successfully convince investors to lean in on a deal. They’re going to board the plane with the expectation that they will soon be skydiving!

They’re excited enough to take the crazy jump and invest.

If a founder is doing their job, they'll take off in the plane with interested investors and execute an organized process. They’ll keep them excited as the plane is climbing. They’ll communicate clearly that we’re all doing this together and there’s only amazing times ahead.

Then it’s

3...

2...

1...

JUMP!

It's exciting. It's exhilarating. Investors are happy to take that leap of faith.

If a founder doesn’t run a tight process, this is when time will absolutely destroy a deal. A plane taking too long to climb and circle around will naturally lead to apprehension. “How many people have died skydiving EVER??” “What happens if the parachute doesn’t deploy?” “Do you know CPR!!?”

If that investor is left to sit in the plane thousands of feet above the earth contemplating the jump, the only things that will enter their mind are the reasons they shouldn't jump.

This is the same in a fundraising process. After an investor becomes interested in a deal, if you give them too much time with no positive updates or continuous momentum, time will kill your deal. The extra time will just be an opportunity to hear about potential risks and question their gut. Giving too much time is just inviting an investor to say “I don't want to jump anymore…”

Look out for next week's post, where we'll walk through a real-world example of this + mistakes to avoid

Small asks!

If you thought this was helpful or enjoyable in anyway, I’d love for you to:

Forward this newsletter with others who would enjoy it

Follow me on Twitter where I’ve begun building in public (my course, my podcast, etc)!

Listen with a friend to Funded, my podcast that tells the rollercoaster stories of how founders raised millions (and subscribe🙏)

Ask me your fundraising questions so I can help you and cover them in a future issue

Thanks for reading Adamant! Subscribe for free to receive new posts and support my work.